Total irregularities in Ghana public sector amount to over GH¢17b – Auditor-General’s Report

Irregularities increased by 135.1% in 2020

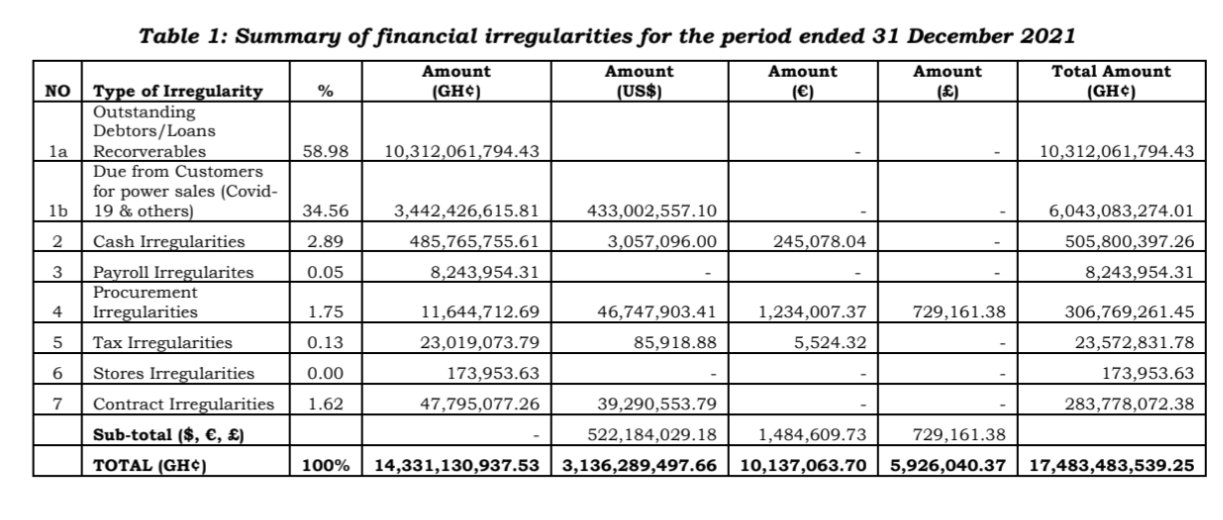

The Auditor-General’s Report on the public sector has recorded irregularities totalling more than GH¢17 billion for the year ending December 2021. The auditors looked into the accounts of Public Boards, Corporations and other Statutory Institutions.

The Auditor-General’s Report on the public sector has recorded irregularities totalling more than GH¢17 billion for the year ending December 2021. The auditors looked into the accounts of Public Boards, Corporations and other Statutory Institutions.

According to the report, the total irregularities stood at GH¢17,483,483,539.25 which included $522,184,029.18 converted into cedis at the prevailing exchange rate of GH¢6.0061 to $1 as at December 31, 2021, €1,484,609.73 converted into cedis at the prevailing exchange rate of GH¢6.8281 to €1 as at December 31, 2021 and £729,161.38 converted into cedis at the prevailing exchange rate as at December 31, 2021.

The report notes that the total irregularities figure of GH¢12,002,880,339 for 2017 decreased to GH¢3,007,258,924 in 2018, however, the irregularities increased by GH¢2,461,139,507 in 2019 to GH¢5,468,398,431.

In the year 2020, the total irregularities also increased by 135.1 per cent from the 2019 figure of GH¢5,468,398,431 to GH¢12,856,172,626. The Auditor-General did not assign any reason to the astronomical increase, but it should be noted that 2020 was an election year.

The report indicates further that during the period ending December 31, 2021, the total irregularities recorded a 36.0 per cent or GH¢4,627,310,913 rise from GH¢12,856,172,626 in 2020 to total irregularities figure of GH¢17,483,483,539.

The increase the report said was occasioned mainly by credit power sales of GH¢6,043,083,274.01 to VRA and NEDCo customers. Overall, however, the report states that, most of the irregularity categories decreased in 2021 compared to the 2020 financial year even though 101 Institutions were audited and reported on in 2021 as compared to the 83 Institutions audited in 2020.

Outstanding Debts/ Loans Recoverable/Credit Power Sales – GH¢16,355,145,068 8. These irregularities represent trade debtors, staff debtors and outstanding loans and cash locked up in non-performing investments. Included in this figure are GH¢4,764,760,731.41 due from customers of Volta River Authority (VRA) and GH¢1,278,322,542.60 due from customers from Northern Electricity Distribution Company (NEDCo) for power supplies in respect of Forex Power Sales, Local Power Sales, Mines Power Sales, Government MDAs’ Power Sales, and GoG COVID-19 Power Relief as at December 31, 2020.

Outstanding Debts/ Loans Recoverable/Credit Power Sales – GH¢16,355,145,068 8. These irregularities represent trade debtors, staff debtors and outstanding loans and cash locked up in non-performing investments. Included in this figure are GH¢4,764,760,731.41 due from customers of Volta River Authority (VRA) and GH¢1,278,322,542.60 due from customers from Northern Electricity Distribution Company (NEDCo) for power supplies in respect of Forex Power Sales, Local Power Sales, Mines Power Sales, Government MDAs’ Power Sales, and GoG COVID-19 Power Relief as at December 31, 2020.

“The absence of effective debt collection policies, non-existence of credit controls to recover the debts and Managements’ indifferent posture towards loan recovery contributed significantly to these conditions,” the report’s authors said.

The auditors also pointed out improper maintenance of records on debtors, the absence of debtors’ ageing analyses, non-documentation of agreements stipulating the terms and conditions of loans, failure to ensure that loans are repaid and Management’s non-compliance with rules and regulations accounted for these irregularities.

The Auditor-General therefore recommended that Management of Public Boards, Corporations, and other Statutory Institutions should strictly adhere to rules and regulations with regards to debts management.

“They should also put in place proper policies for the management of loans and other receivables as well as ensuring that loans and debts are repaid on due dates to avoid or minimise the occurrence of bad debts,” the government auditor recommended.

On cash irregularities related to the misapplication of funds, budget overruns, payments not authenticated and payment of Board Allowances to Council Members without Ministerial approval, the report found that out of the total figure of GH¢505,800,397 cash irregularities, GH¢230,700,424.38 represented unbudgeted expenditure by the Ghana Cocoa Board on the principal repayment of a ten-year loan with the Bank of Ghana (BoG) which was not included in the approved budget for 2019/2020 financial year.

These, the report said, occurred because of poor oversight responsibility and nonexistent controls.

“Other contributory factors were finance officers’ failure to properly file and keep records, Management’s failure to ensure the security and safety of vital documents, non-maintenance of returned cheque registers, Management’s inertia in complying with procedures stipulated in the Public Financial Management Act, and poor accounting systems,” it added.

Payroll Irregularities – Amounted to GH¢8,243,954.13. These lapses were caused by the failure of Management to exercise due diligence, and the tolerance of officers in charge of payroll validation in reviewing payment vouchers to ensure salaries were paid to only those who were entitled as well as payroll related irregularities.

“They were also caused by Management’s failure to notify banks to stop the payment of unearned salaries. The Controller and Accountant-General’s Department also did not promptly delete names of separated staff when notified to do so. In other instances, Management also did not transfer statutory deductions in respect of PAYE taxes and SSF contributions,” the report said.

The report notes that contained in the total irregularity of GH¢8,243,954 is an amount of GH¢2,992,444 attributed to the Ghana Broadcasting Corporation in respect of avoidable pending judgement debt due to the termination of appointment of a former Director-General, judgement debt for the failure to pay long service award to employees, payment of unearned salaries and the late payment of 1st and 2nd tier pension contributions.

The report found Procurement Irregularities amounting to GH¢306,769,261 16. These irregularities the report indicated, occurred as a result of Managements’ non-compliance with the provisions of the Public Procurement Act, 2003 (Act 663) as amended. Out of the total irregularities, GH¢ 219,350,277.98 represented items procured without recourse to the Public Procurement Authority (PPA) by the Electricity Company of Ghana, it said.

The report found tax irregularities of GH¢23,572,832 18 related to failure to pay statutory tax deductions on due dates, and non-deduction of applicable taxes. They also related to transacting business with non-VAT registered persons or entities.

“Out of the total tax irregularities of GH¢23,572,832, an amount of GH¢23,196,270.05 was attributed to Electricity Company of Ghana (ECG) for delayed remittance of P.A.Y.E and withholding taxes and the non-deduction of withholding taxes and withholding VAT,” it noted.

The Auditor-General also found stores irregularities totalling GH¢173,954 20. These irregularities it said, included non-documentation of store items, lack of awareness of officers assigned to store duties and inadequate supervision. Included in the sum of GH¢173,954 is an amount of GH¢58,698.63 worth of unused conductor cables not recovered from Contractors into the Stores of the Electricity Company of Ghana.

The auditors found contract irregularities in the amount of GH¢283,778,072 22, and these mainly relate to the payment for construction projects not undertaken by various Public Boards, Corporations and other Statutory Institutions. Included in the irregularities figure of GH¢283,778,072, is an amount of $36,890,553.79 (GH¢221,568,355) paid by the Social Security and National Insurance Trust (SSNIT) to a contractor in excess of work performed on a project.

By Emmanuel K Dogbevi