To Ghana government: Delay Agyapa minerals royalty agreement to allow broader consultation

Introduction

Introduction

Ghana’s public space over the past fortnight has been pre-occupied with the debate on the mineral royalties investment agreement – herein called the ‘Agyapa Deal’. There have been several calls by civil organisations, respected statesmen and ordinary citizens for government to hasten slowly on the ‘Agyapa Deal’. Reasons cited include the “lack of full disclosure on the beneficial ownership of the Special Purpose Vehicle”[1], how setting up in “a tax haven sends a bad signal to the players in the country’s minerals value chain”[2], and why “it is not good to use the nation’s resources to leverage our assets for tomorrow”[3], among others.

Under the agreement, the sovereign State of Ghana intends to monetise parts of its annual gold royalties from some mining concessions to purportedly raise $500 million of equity (upfront cash) from private investors through the placement of shares in a newly created entity (Special Purpose Vehicle: SPV) which the Ghanaian State will transfer its royalties into – more on this later. Ghana’s finance minister, Ken Ofori-Atta, on 27 August announced at a press briefing that the Agyapa Mineral Royalty arrangement “was the best deal for Ghana’s gold”.[4] Deputy Minister for Finance, Charles Adu Boahen further asserts that “the main purpose [of Agyapa] was to offer financing to gold mining companies that wanted to develop new mining projects in exchange for royalties or revenue once the mines started producing gold.“[5] He also asserted that “[critics] don’t really understand the transaction”.[6]

The idea of utilising other innovative approaches in raising money is not bad, and neither is it illegal; it is a way for the State to raise relatively cheap money or interest-free money, and to create more value in the mining value chain. In essence, what the government is seeking to do is to swap one set of future cashflows (mineral royalties) due to the sovereign State of Ghana from its interests in mining concessions/leases with another set of cash flows, mostly dividends in addition to the upfront capital. This is done via the placement of shares or IPO for private individuals to own shares in the new commercial entity (SPV).

However, there are significant concerns around valuation, governance and the wider transformation plan for the mining (extractives) sector, which I explain in the next sections, starting off with the Agyapa structure and principal parties.

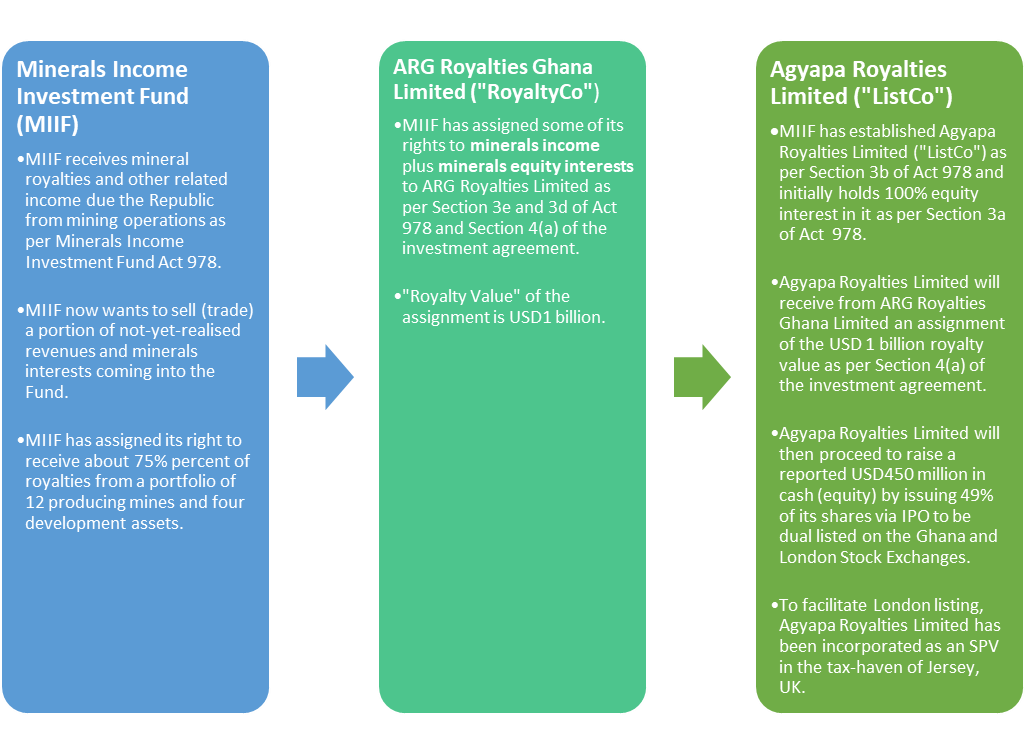

Agyapa Structure and Principal Parties

The principal parties to the agreement are as follows:

- The Republic of Ghana, acting through and represented by the Ministry of Finance (the “Republic”)

- The Minerals Income Investment Fund (the “Fund”)

- ARG Royalties Ghana Limited (“RoyaltyCo”); and

- Agyapa Royalties Limited (“ListCo”)

The figure below outlines the relationships among the principal parties and transaction flows. The Positives

The Positives

Essentially, what I gather from the documentation and information available is that the State is saying minerals royalties are relatively too small given plans to invest in owning additional mines and value chain infrastructure such as processing hubs, new geological discoveries and haulage infrastructure. Hence, innovative approaches are required to raise more financing for mining infrastructure investment to get a larger share of mining proceeds without burdening the public purse. Traditionally, the government would have gone to borrow to finance such capital investments and or used the royalties as a guarantee to pay off these investments – an example of this is current Bauxite swap model we have with China.

Therefore, government seeks to monetise relatively safer royalties to raise an initial $500 million in cash through offloading of 49 per cent of shares (equity) in Agyapa Royalties Limited (“ListCo”) in both Ghana and the United Kingdom. The listed shares would trade on an exchange, increasing or decreasing in value through the actions of the market on the underlying asset, which is gold. To facilitate its London listing, Agyapa Royalties Limited has been incorporated as a Special Purpose Vehicle (SPV) in the tax-haven of Jersey, UK. It is important to note that SPVs are used every day in international financial markets, mostly as bankruptcy remote entities in structured finance transactions to tap money from investors.[7] Under the SPV, the State’s contribution to the new company is its equity investment via the minerals income and mining interests.

In contrast, private shareholders are also contributing equity by buying shares in Agyapa Royalties Limited. The value of their shareholding will rise or fall depending on market fundamentals. In the event of an increase in the price of gold, for example, all shareholders would benefit from cash dividend payout. The government would receive the $500 million upfront while limiting itself to any downside exposures but reaping the upside via the market capitalisation when gold prices go up. So, the proposed 51 per cent of that royalty will come back to government through its shareholding. Also, government could go back to the market to raise additional funds through buybacks or bond issuances, among others. The approach is not bad in theory, and it’s not uncommon.

Concerns

Below, I outline the significant issues that need further attention or clarification from the government on the valuation, governance and wider transformation plan before proceeding.

- Valuation & Related Matters

Under Section 3.1 of the Amended Investment Agreement (AIA), MIIF will assign all its rights and privileges as well as pay its royalty share into Agyapa Royalties over the duration (term) of the agreement (Section 2.2 of AIA). Under Section 4 of AIA, on what fair value analysis was the USD 1 billion valuation (“royalty value”) arrived at? Is this based on cash flow or price-to-earnings (PE) valuation? An off-the-hand cash flow calculation using an average USD 150 million royalty receivables per annum based on historical trends, then extrapolating this over 15 years and discounting at 5%, yields a net valuation of USD1.6 billion in present value (PV) terms. This increases to USD2.1 billion based on USD 200 million annual royalty receivables. Of course, nobody can forecast where gold prices are likely to be in the future. However, a reasonable estimate is needed to arrive at a possible valuation to guide share pricing. Also, according to the Deputy Finance minister’s 29 August JoyFM Newsfile appearance, the USD1 billion “royalty value” as stated in Section 4(a) the amended investment agreement is the “share capital” of the RoyaltyCo (ARG Royalty) and not the underlying valuation of the mineral royalties, the latter which the market will determine. So, the market capital will be determined on day one (1) of trading. Given the above statement, it is thus conceivable that the actual shareholding structure in consideration for raising USD 500 million via the IPO could be more significant for the State. For example, raising USD 500 million cash through equity injection in return for the future mineral income and mineral rights would translate into 31.25%:68.75% shareholding split between the private investors and the government, based on an assumed $1.6 billion valuation. Perhaps further details will be made available in the IPO prospectus.

This raises a second question: why do we want to lock ourselves into a 15-year plus agreement? In any case, the proposed $500 million that the government seeks to raise is equivalent to about three years’ worth of minerals royalties at current prices so why does the State want to give away not only the minerals income but the rights and associated flexibility options? In effect, what is the opportunity cost of foregone royalties to other future governments? Is it just a question of raising money, or is there a broader development agenda through the creation of a quasi-Sovereign Wealth Fund (SWF) via Agyapa Royalties? Thirdly, is there a guaranteed share buy-back option by the government (MIIF), once the investors have recouped their investment after some period? Fourthly, regardless of any bankruptcy remote provisions or caveats, can the private shareholders, exercise their right to the underlying asset, which is Ghana’s minerals equity interests for the duration of the respective contracts if something goes awry? For example, in the event of SPV liquidation arising out of poor management and investment decisions. Again, this does not preclude the fact that in event of liquidation, shareholders will be last to be paid given that the pecking order remains bondholders, preferred shareholders and then ordinary shareholders.

The above are serious issues that require further policy considerations or at least some detailed explanation from the government.

- Governance (Tax jurisdiction)

The argument raised within some quarters of SPV tax jurisdiction being in Jersey is neither here nor there so long as accounting and fiduciary protocols are followed. By the dual listing on the LSE and GSE, one can anticipate that all governance and anti-money laundering protocols are likely to be followed. The is backed up by Section 36—Transparency as a fundamental principle of Act 978, specifically 36(2) and 36(3) which enjoins the management to be carried out “in accordance with the highest internationally accepted standards of transparency and good governance” and “to entrench transparency, accountability and free access by the public to information.” Also, as per Section 35 of Act 978 – “the mineral income paid to the Fund and the dividend payable by the Fund or a Special Purpose Vehicle are not taxable.” Hence, by registering in Jersey, this circumvents the prospects of the shareholders having to pay capital gains and other taxes to the UK government, thus retaining more value for all parties. Nonetheless, it is important that the identities of the beneficial owners of any companies or shell entities which buy into the IPO, when it is eventually listed, are disclosed as a matter of principle. This can be done for all shareholders with more than 3 per cent shares to reduce administrative burden.

Any lack of transparency in governance can hurt well intended capital raising initiatives such as this. A good case study is Malaysia’s recent experience.[8] 1Malaysia Development Berhad (1MDB) started off as Terengganu Investment Authority (TIA). TIA was a Sovereign Wealth Fund (SWF) with an initial fund of RM11 billion ($2.6 billion) aimed at ensuring the economic development of Terengganu state. Outstanding royalty income of RM6 billion ($1.4 billion) and funds from bond issued by local and overseas financial markets was used to set up TIA. This includes the Malaysian Federal Government proposing to provide RM5 billion guarantee based on TIA’s future oil revenues. Financial oversight and auditing of the fund was taken from the government’s Auditor General of Malaysia and handed over to private firms. However, between 2009 and 2013, the fund had changed its auditors three times raising red flags among the country’s opposition members of Parliament. Due to the public discontent over the lack of transparency with the funds account, the Prime Minister in 2015 ordered the audit of 1MDB by the Auditor General of Malaysia. The final report was classified state secret until it was declassified in 2018. The US justice department believes more than $4.5 billion was stolen.[9] 1MDB will go on to become one of the global finance sector’s biggest money laundering scandals in modern times with rippling effects running through Hollywood to Hong Kong. The aftermath of the scandal saw Malaysia’s former prime minister Najib Razak facing multiple corruption charges and his coalition party losing the elections, ending their six-decade hold on power.[10]

- Transformation plan

Perhaps, the most critical question in this whole public debate which has not been addressed is this: what is the strategic or transformation plan for the MIIF and the mining sector? There are conflicting statements I have cited on the purpose of raising the monies. This includes, among others, that: (1) the funds realised are expected to be re-invested in the mining sector of Ghana and other countries in the sub-region; (2) funds would be used to support the government’s infrastructure drive and budgetary needs. Concerning the latter point, Section 4(3) of MIIF (Functions of the Fund) states that “in the performance of its functions, the Fund or SPV shall not provide credit to the government, public enterprises, private sector entities or any other person or entity”. Basically, the letter and spirit of the Fund/SPV is to operate as pure commercial going concern, which generates profits back to the State.

It is within this vein that I think the government must be forthcoming on the plan regarding what it would be investing the monies raised in and how it generates future profits. Which investments would the government be undertaking with the monies? Are these projects economical to breakeven and generate some rents on their own terms? Will it finance social (hospitals) or more critical economic infrastructure (railways and roads connected to minerals value chain)? Are these investments anchored on a long-term national infrastructure plan? Ghana has a history of several grandiose white elephant projects that have failed due to ineffective planning. Countries grow because they not only borrow but invest in productive assets.

Hence, the success of the purported attempts at state-led industrialisation, this time with private market participation will most importantly depend on full transparency on the SPV’s operations, the investment processes by which funds raised are deployed in productive assets.

Way Forward

- I would suggest that the government should temporarily suspend the deal to allow further consultation; this is because I don’t see the need to rush this, and besides, it is too close to the December 2020 elections to allow proper scrutiny. This considers the fact that Parliament has passed the amended agreement as of August 14, 2020, and the conditions precedent for listing the securities of the London Stock Exchange need to happen on or before December 31, 2020. The stock exchange will always be there, and gold prices aren’t coming down considerably anytime soon, at least not in the next few months given the COVID-19 pandemic where it has become a store of intrinsic value.

- An option worth considering would be for the government to sell the rights to the royalties to a minerals income fund for an initial five-year period in return for an upfront $500 million cash payment being considered. The monies will be serviced with royalty payments placed in an Escrow account; this ensures that we will meet repayment schedules. This is cleaner, less complex and easier to manage without encumbering future governments. The current proposed approach creates additional complexity and more players in the food chain by way of lawyers, asset managers and accountants, many of whom must be paid annual retainer fees running into millions of dollars. That’s an implied interest rate or cost of borrowing.

- It is important that the identities of the beneficial owners of any companies or shell entities which buy into the IPO, should they be eventually listed, are disclosed as a matter of principle. This can be done for all shareholders with more than 3 per cent shares to reduce administrative burden.

- Should the government decide to proceed with the current listing, then I would suggest that the greater majority of the monies must be raised locally if possible, to boost our capital markets. This would allow both Ghanaian institutional shareholders including GIIF, SNNIT and Pension Funds as well as ordinary citizens to own most of the shares, thereby benefiting from the upside.

- Government should create a national infrastructure working group and standards body (or utilise the National Development Planning Commission: NDPC) which will determine which infrastructure the country needs and where; how much money do we need, and update the costings every two to three years. Money is just one part of the problem. Going for $500 million or $1 billion when there are too many leakages and no clear roadmap is risky. Ghana’s history is replete with the failures of such good intention initiatives like Rawlings’ divestiture programme to fund infrastructure. Execution is key.

- Finally, the government should issue a simple key explainer document/white paper/background paper about the MIIF and the rationale/policy imperatives for the creation of Agyapa Minerals Ltd. The deep mistrust for our governments and political officials is often due to the lack or unavailability of critical information. Little wonder that some 15 CSOs have demanded a suspension of the agreement until all necessary documents have been disclosed.

By Dr. Theo Acheampong

Dr Theophilus Acheampong is an energy economist and political risk analyst with expertise in providing economic and investment analysis as well as research and strategic advisory in the extractives industry and public finance. His work focusses on regulatory and commercial issues within the upstream oil and gas, power and downstream energy industry, including in fiscal regime modelling, contractual negotiations, hydrocarbon accounting, and economic policy analysis.

Sources:

[1] https://citinewsroom.com/2020/08/critics-of-agyapa-royalties-deal-lack-full-understanding-adu-boahen/

[2] https://www.myjoyonline.com/news/national/agyapa-royalties-deal-sends-terrible-signal-to-industry-players-africa-centre-for-energy-policy/

[3] https://www.mofep.gov.gh/news-and-events/2020-08-29/agyapa-royalties-best-deal-for-ghana%E2%80%99s-gold-ken-ofori-atta

[4] https://www.mofep.gov.gh/news-and-events/2020-08-29/agyapa-royalties-best-deal-for-ghana%E2%80%99s-gold-ken-ofori-atta

[5] ibid

[6] https://citinewsroom.com/2020/08/critics-of-agyapa-royalties-deal-lack-full-understanding-adu-boahen/

[7] https://www.sidley.com/-/media/publications/ljns-equipment-leasing-newsletter–august-2017.pdf?la=en

[8] https://www.theguardian.com/world/2018/oct/25/1mdb-scandal-explained-a-tale-of-malaysias-missing-billions

[9] https://www.justice.gov/opa/pr/us-seeks-recover-approximately-540-million-obtained-corruption-involving-malaysian-sovereign

[10] https://nypost.com/2018/05/10/malaysias-new-prime-minister-is-the-worlds-oldest-elected-leader-at-92/