Compliance with IMF programme credit positive for Ghana – Moody’s

The credit ratings agency Moody’s broadly meeting the International Monetary Fund’s (IMF) programme targets for 2015, is credit positive for Ghana.

The credit ratings agency Moody’s broadly meeting the International Monetary Fund’s (IMF) programme targets for 2015, is credit positive for Ghana.

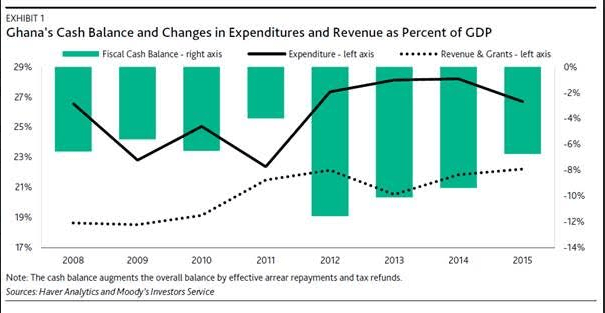

In a report authored by Elisa Parisi-Capone, Moody’s Vice President – Senior Analyst, and copied to ghanabusinessnews.com, Moody’s said in addition to broadly meeting the performance criteria under its $918 million three-year Extended Credit Facility (ECF) programme, the year-end 2015 fiscal deficit of 6.7 per cent of GDP in cash terms surpassed the budgeted 7.0 per cent target and marked a significant improvement from the 9.4 per cent deficit reported in 2014, and the country’s fiscal consolidation efforts included larger-than-expected arrear repayments.

The IMF on April 3, 2015, approved a $918 million three-year ECF for Ghana, but classified the country as “high risk of debt distress” under a new debt sustainability analyses (DSA).

Moody’s notes that the continued compliance with the IMF programme criteria is credit positive because it bolsters investor confidence amid difficult domestic and external funding conditions.

Moody’s states that revenue and expenditure data indicate that Ghana is making progress on both.

At 22.2 per cent of GDP, year-end revenues and grants exceeded the budgeted amount by 0.4 percentage points of GDP, whereas expenditures of 26.7 per cent of GDP constituted savings of 0.5 percentage points.

“That said, higher-than-projected import revenue exemptions of 1.5 per eent of GDP point to significant foregone revenues mainly related to large investments in the oil, gas and power sectors. The Ministry of Finance has announced greater oversight in granting exemptions, and will work with the IMF to broaden Ghana’s tax base and increase tax revenues, which, although improving, remains constrained at 17.3 per cent of GDP,” it says.

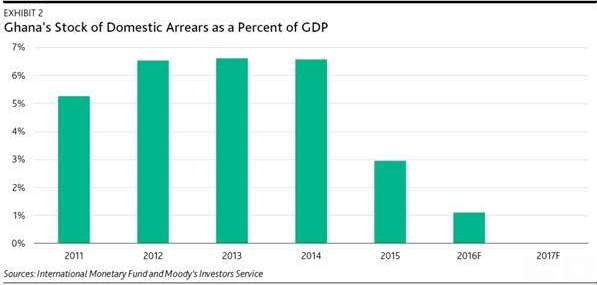

According to Moody’s an important achievement in Ghana’s fiscal consolidation process is the accelerated clearance of accumulated domestic arrears, which reached a peak of about 6.5 per cent of GDP in 2014.

At the end of 2015, effective arrear repayments and tax refunds amounted to 2.4% per cent of GDP, versus a budgeted 1.7 per cent. The government aims to clear another 1.4 per cent of GDP this year and the remainder by the end of 2017 without incurring any new domestic arrears, in line with one of the programme’s quantitative benchmarks.

“The outstanding amounts include arrears to utility companies, other state-owned enterprises, statutory funds, the pension fund and audited claims by oil importers related to foreign-exchange losses in 2014 and early 2015,” it adds.

The agency however, notes one concern raised by the IMF. It indicates the one exception the IMF cited, and calls it, “the small overstep in the wage bill.” It says the wage bill is at an effective 7.5 per cent of GDP from 8.3 per cent in 2014, versus a nominal ceiling equal to 7.4 per cent of GDP.

“Gradually, more stringent payroll controls introduced in April 2015 have contributed to reducing the wage/tax revenue ratio to 43.7 per cent in 2015 from 49.1 per cent in 2014 and almost 65 per cent in 2012. We expect the level to decline to the government’s stated target of 35 per cent after 2017,” it adds.

Commenting on the funding side, Moody’s says the fiscal deficit and large rollover needs, especially in the domestic debt market, result in public gross financing needs of about 20 per cent of GDP in 2016 and in 2017, when a $530 million Eurobond matures.

“Taking into account the tight domestic and external funding conditions, the government has underscored its commitment to continued fiscal consolidation during the current election year by offsetting any oil revenue shortfalls arising from the $53 oil price assumption in the 2016 budget, and by adding further safeguards against potential wage bill overruns to achieve the revised cash deficit target of 4.8 per cent of GDP from 5.3 per cent previously,” Moody’s says.

The agency however, clarifies that the report does not contain any credit rating actions and does not change Ghana’s existing B3 (Negative Outlook) government bond rating.

By Emmanuel K. Dogbevi